MarketSenseAI 2.0: Enhancing Stock Analysis through LLM Agents

题目: MarketSenseAI 2.0:通过 LLM 代...

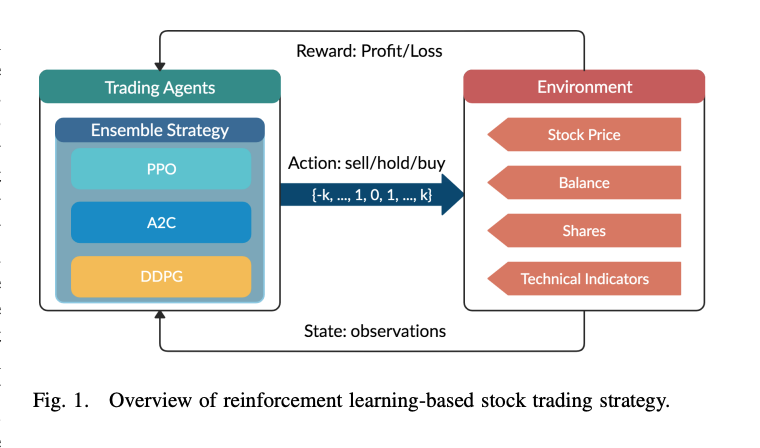

题目: 自动化股票交易的深度强化学习:一种集成策略。

作者: Hongyang Yang、Xiao-Yang Liu、Shan Zhong、Anwar Walid(2025)。

摘要要点: 本文提出由策略梯度、actor-critic、值基混合等多种深度 RL 代理组成的集成体,并设计一个元学习的集成管理器,根据市场状态信号动态分配各代理权重。通过消融实验与考虑真实交易成本的回测,展示该集成策略在收益稳定性和回撤控制上优于单一 RL 代理与传统策略。

Deep Reinforcement Learning for Automated Stock Trading: An Ensemble Strategy

Authors: Hongyang Yang, Xiao-Yang Liu, Shan Zhong, Anwar Walid — 2025.

Source / arXiv (PDF): arXiv:2511.12120 (Nov 2025 preprint).

English summary: The paper presents an ensemble of complementary deep RL agents (policy-gradient, actor-critic, and value-based hybrids) that learn diversified trading rules and an ensemble manager that meta-learns allocation among agents based on market regime signals. They provide extensive ablation studies, realistic trading cost models, and demonstrate that the ensemble outperforms single-agent RL and classical strategies in return consistency and drawdown control. (PDF available on arXiv).